Date : 29.5.2020

A very good morning boys

Today we will be doing the main market forms.

Market refers to the whole region where buyers and sellers of a commodity are in contact with each otherto effect purchase and sale of a commodity.

There are two main forms of Market Structure

1. PERFECT COMPETITION

2. IMPERFECT COMPETITION :

The Imperfect Competition market form is divided into three parts

- Monopoly

- Monopolistic Competition

- Oligopoly

PERFECT COMPETITION: Perfect Competition refers to a market situation where there are very large number of buyers and sellers dealing in a homogeneous product at a price fixed by the market.

In a Perfectly Competitive market, sellers sell a homogeneous product at a single uniform price.This Price is not determined by a particular firm but by the Industry.

In reality, perfectly competition has never existed.

Features of Perfect Competition

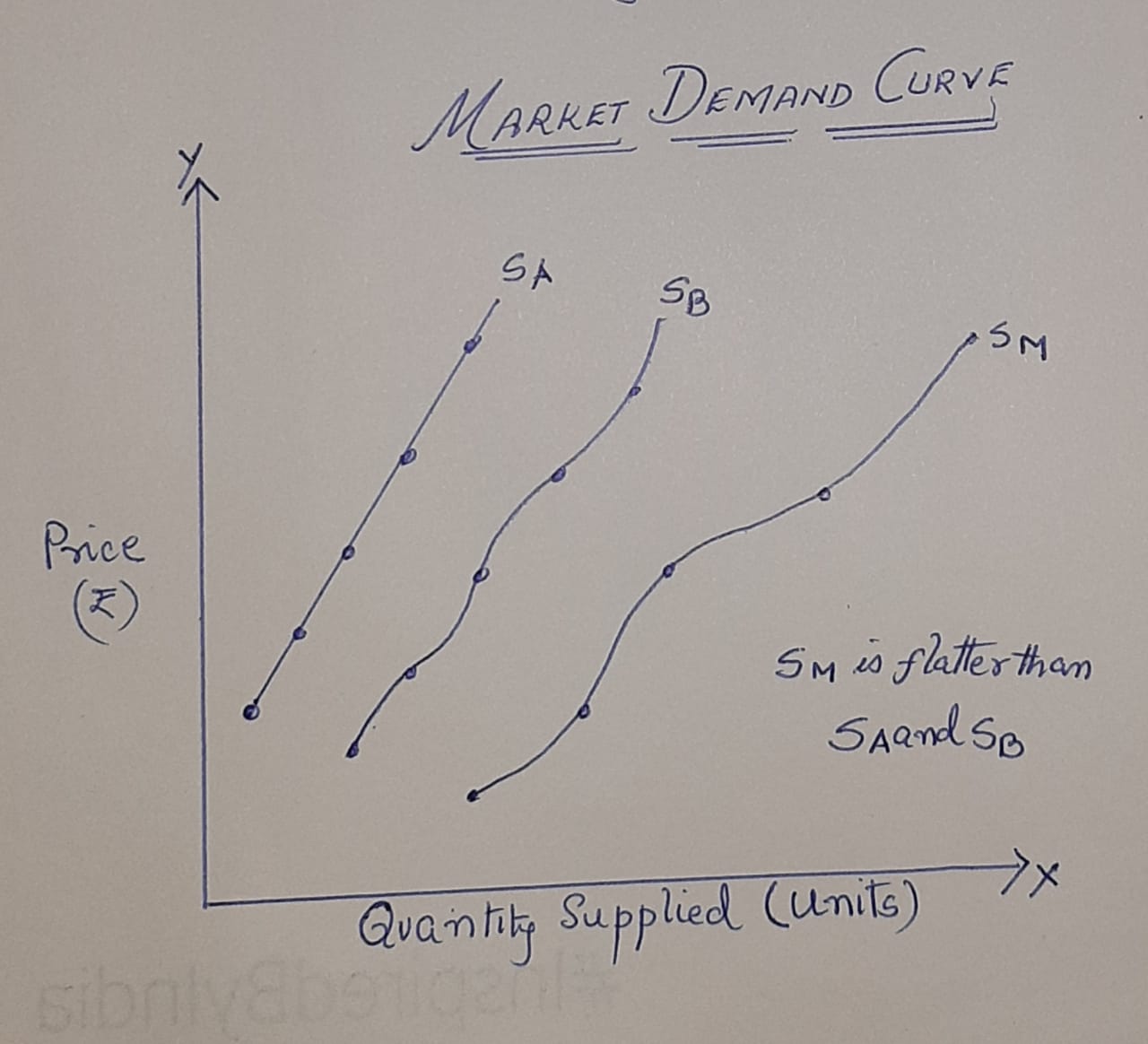

1. Very Large Number of Buyers and Sellers : There are a very large number of buyers and sellers.

Implication: Very Large number of buyers and sellers is that the number of sellers is so large that the share of each seller is insignificant in the Total supply.It is the same case with demand with the buyers.

2. Homogeneous Product : The product for sale is identical in all respects like shape, size,quality, color,etc.

Implication: No individual firm is in aposition to charge a higher price for a product as the products are identical in all respects.

3. Freedom of entry and Exit: Every seller has the freedom to enter and exit the Industry.There are no artificial natural barriers for entryof new firms and exit of existing firms.It ensures absence of abnormal profits and abnormal losses in the long run.

Implication: Firms will only earn normal profits in the long Run.

UNDER PERFECT COMPETITION DEMAND CURVE IS A HORIZONTAL STRAIGHT LINE PARALLEL TO THE "X" AXIS

MONOPOLY: refers to a market situation where there is a single seller selling a product which has no close substitutes. Ex Railways in India

Features of Monopoly

1. Single Seller : Monopolist has full control over the supply and price of the product.No single buyer can influence can influence the market price.

2. No close substitutes: Thus, he has no fear of competition from new or existing products.

3. Restriction on Entry and Exit: As a result it earns (abnormal profits/abnormal losses) in the long runlong run .

4. Price Discrimination: Charging different prices for the same product.

UNDER MONOPOLY THE DEMAND CURVE IS SLOPING DOWNWARD

Monopolistic Competition: refers to a market situation in which there are large number of firms which sell closely related but differentiated goods.Ex- Soaps, Toothpaste, etc

Features of Monopolistic Competition:

1. Large number of Sellers: Large number of firms selling closely related, but not homogeneous products.

2. Product Differentiation: refers to differentiating the product on the basis of brand, size, colour,etc.

3. Selling Cost: refers to expenses incurred on marketing, sales promotion and advertisment of the product.

UNDER MONOPOLISTIC COMPETITION THE DEMAND CURVE IS DOWNWARD SLOPING WITH THE ONLY DIFFERENCE THAT IT IS MORE FLATTER THAN THE DEMAND CURVE OF MONOPOLY MARKET.

Oligopoly: refers to a market situation in which there are few firms selling homogeneous or differentiated products.

It is also known as competition among the few

Features of oligopoly

1. Few Firms : There are a few large firms.Exact number is not defined.Each producer produces a significant portion of the total output.Ex- automobiles

2. Interdependence: Each firm is mutually dependent on the decision of its rival firm regarding price and output decision.

3. Non Price Competition: The firms dont practise Price discrimination but practise non price discrimination such as free insurance for a year, free gifts,etc

Dear boys i have put 4 videos for each market form respectively.

Make sure you watch them carefully to understand the topics better