Date: 28.5.2020

A very good morning students

Today we move to the next chapter which is cost.

Let us first understand a few important terms

COST: Cost in economics includes actual expenditure on inputs ( explicit cost) and the imputed value of the inputs supplied by the owners(implicit cos

Explicit Cost : It is the actual money expenditure on inputs or payment made to outsiders for hiring their factor services.Ex- Wages paid to employees

Implicit Cost : It is the cost of the self supplied factor of production.Ex- Slary for the service of entrepreneur

Thus, we can say that COST= Explicit Cost+ Implicit Cost

Cost Function : The relation between cost and output is known as 'Cost Function'

It refers to the functional relationship between cost and output

It is expressedas C = f(q)

Oppurtunity Cost : Oppurtunity Cost is the cost of the next best alternative forgone.

Short Run Cost: We know , in Short Run , some factors which are fixed, while others are variable.

Similarly, short run cost are also divided into two kinds of cost: Fixed Cost and Variable Cost

Sum of Fixed Cost and Variable Cost equals Total Cost

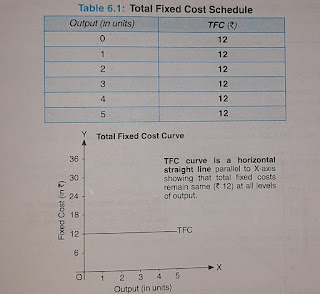

TOTAL FIXED COST(TFC) OR FIXED COST(FC) : Fixed Cost refers to those costs which do not vary directly with the level of Output. Ex- Rent of building,salary of permanent staff,etc

These are cost that cannot be changed in the short run

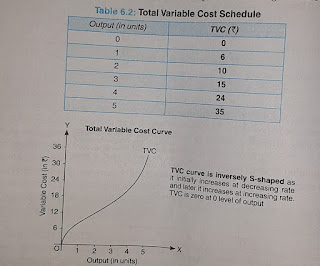

TOTAL VARIABLE COST(TVC) OR VARIABLE COST(VC): Variable cost refer to those costs whichvary directly with the level of output. Ex- payment of raw material,power,fuel,etc.

Such costs are incurred till there is productionand become zero at zero level of output.

TOTAL COST(TC) : Total Cost is the total expenditure incurred by a firm on the factors of production required for the production of a commodity.

TC= TFC+TVC

Since TFC remains same at all levels of output, the change in TC is entirely due to TVC

Relationship between TC,TFC and TVC

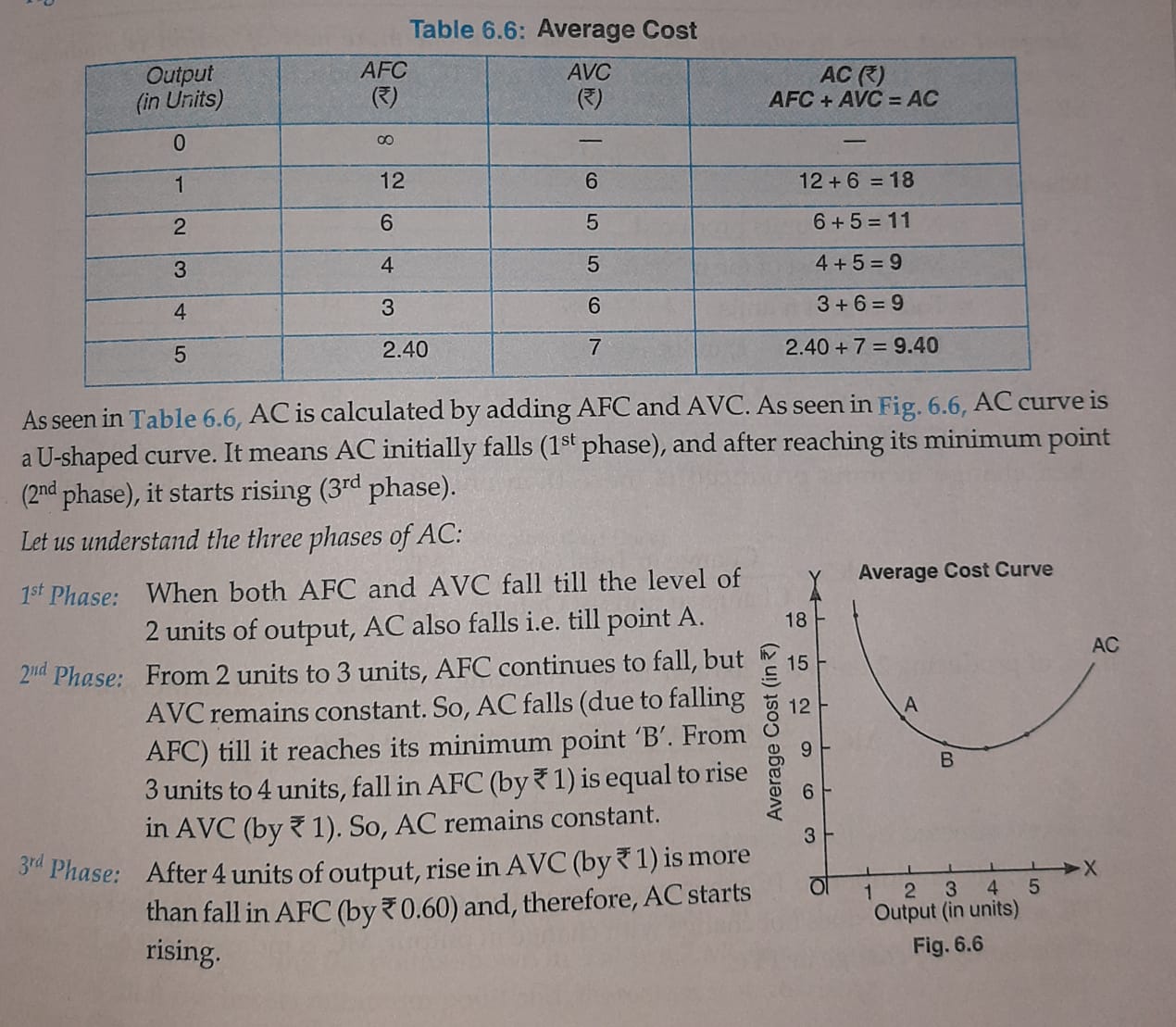

AVERAGE COST:

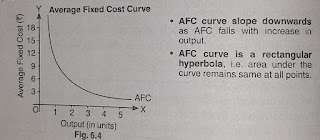

Average Fixed Cost (AFC): Average fixed cost refers to the per unit fixed cost of production.

AFC = TFC/ Q ( Q= Quantity of Output)

AFC falls with increase in output as TFC remains same at all levels of output.

AFC is a rectangular Hyperbola,i.e. area under AFC curve remains same at different points.

AVERAGE VARIABLE COST (AVC) : Average variable cost refers to the per unit variable cost of production.

AVC = TVC/Q (Q= Quantity of Output)

AVC initially falls with increase inoutput. Once the output rises till optimum level,AVC starts rising.It can be better understood with the help of a schedule and diagram given below.

AVERAGE TOTAL COST(ATC) or AVERAGE COST(AC)

Average cost refers to the per unit total cost of production.

AC = TC/Q (Q= Quantity of Output)

Average cost is also defined as the sum of AFC+ AVC

Like AVC, average cost also initially falls with increase in output. Once the output rises till optimum level, AC starts rising. It can be better understood with the help of a schedule and diagram.

MARGINAL COST (MC) : Marginal cost refers to addition to Total Cost when one more unit of output is produced.

MCn= TCn - TCn-1

OR

MC = Change in TC/ Change in units of output

MC IS NOT AFFECTED BY FIXED COST

The reason behind the 'U' shape of MC is the LAW OF VARIABLE PROPORTION.

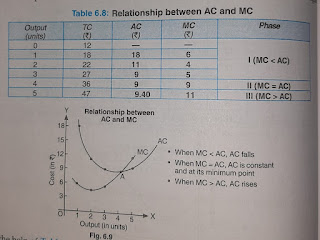

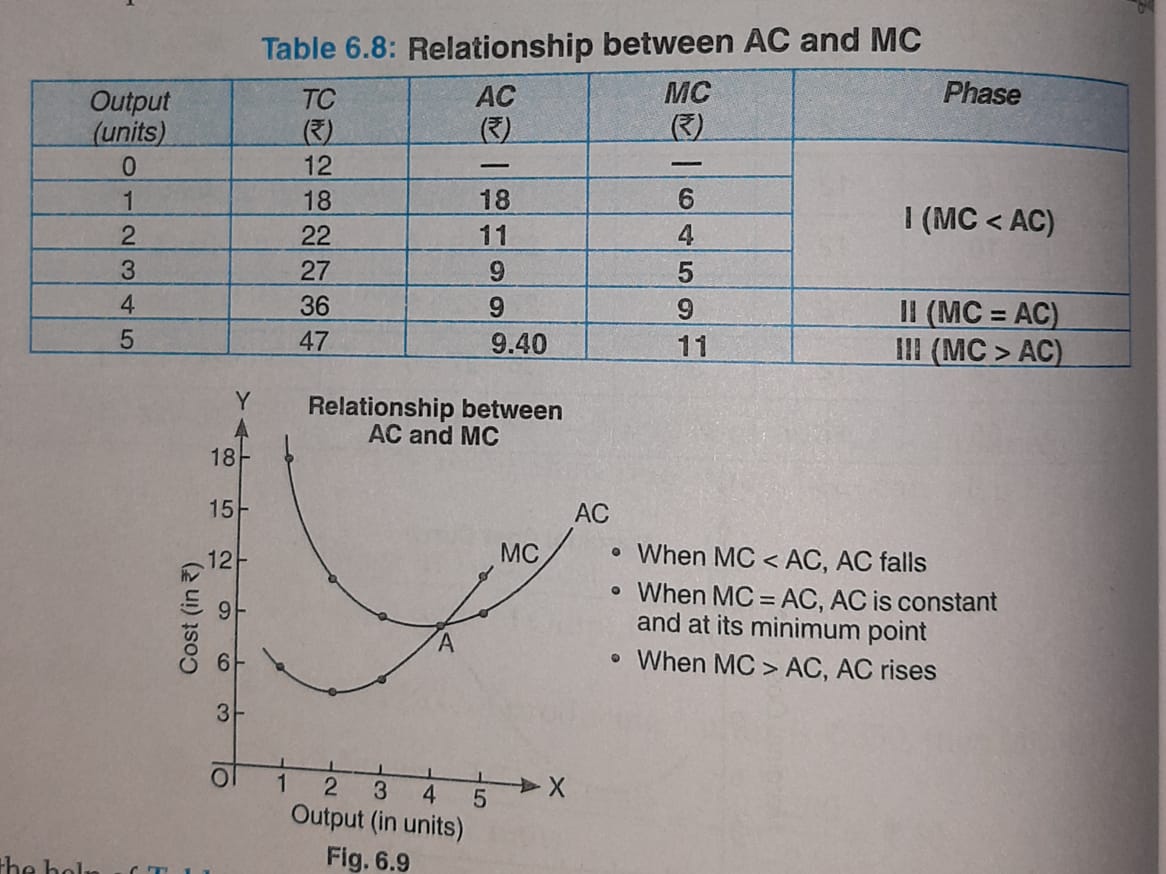

Relation between AC and MC

Please go through the video links to understand the chapter better

https://www.youtube.com/watch?v=xZ6-h9Ib2LE

https://www.youtube.com/watch?v=Yr0eiVdK1RY

https://www.youtube.com/watch?v=uVFPB90gpWM&t=158s

A very good morning students

Today we move to the next chapter which is cost.

Let us first understand a few important terms

COST: Cost in economics includes actual expenditure on inputs ( explicit cost) and the imputed value of the inputs supplied by the owners(implicit cos

Explicit Cost : It is the actual money expenditure on inputs or payment made to outsiders for hiring their factor services.Ex- Wages paid to employees

Implicit Cost : It is the cost of the self supplied factor of production.Ex- Slary for the service of entrepreneur

Thus, we can say that COST= Explicit Cost+ Implicit Cost

Cost Function : The relation between cost and output is known as 'Cost Function'

It refers to the functional relationship between cost and output

It is expressedas C = f(q)

Oppurtunity Cost : Oppurtunity Cost is the cost of the next best alternative forgone.

Short Run Cost: We know , in Short Run , some factors which are fixed, while others are variable.

Similarly, short run cost are also divided into two kinds of cost: Fixed Cost and Variable Cost

Sum of Fixed Cost and Variable Cost equals Total Cost

TOTAL FIXED COST(TFC) OR FIXED COST(FC) : Fixed Cost refers to those costs which do not vary directly with the level of Output. Ex- Rent of building,salary of permanent staff,etc

These are cost that cannot be changed in the short run

TOTAL VARIABLE COST(TVC) OR VARIABLE COST(VC): Variable cost refer to those costs whichvary directly with the level of output. Ex- payment of raw material,power,fuel,etc.

Such costs are incurred till there is productionand become zero at zero level of output.

TOTAL COST(TC) : Total Cost is the total expenditure incurred by a firm on the factors of production required for the production of a commodity.

TC= TFC+TVC

Since TFC remains same at all levels of output, the change in TC is entirely due to TVC

Relationship between TC,TFC and TVC

- TFC curve is a horizontal straight line parallel to X-axis as it remains constant at all levels of output.

- TC and TVC curves are inversely S-shaped because they rise initially at a decreasing rate, then at a constant rate and finally,at an increasing rate.

- At zero output,TC is equal to TFC because there is no variable cost at zero level of output.So, TC and TFC curves start from the same point, which is above the origin.

- The vertical distance between TFC curve and TC curve is equal to TVC.As TVC rises with increase in the output, the distance between TFC and TC curve also goes on increasing.

- TC nd TVC curves are parallel to each other and the vertical distance between them remains the same at all levels of output because the gap between them represents TFC,which remains constant at all levels of output.

Average Fixed Cost (AFC): Average fixed cost refers to the per unit fixed cost of production.

AFC = TFC/ Q ( Q= Quantity of Output)

AFC falls with increase in output as TFC remains same at all levels of output.

AFC is a rectangular Hyperbola,i.e. area under AFC curve remains same at different points.

AVERAGE VARIABLE COST (AVC) : Average variable cost refers to the per unit variable cost of production.

AVC = TVC/Q (Q= Quantity of Output)

AVC initially falls with increase inoutput. Once the output rises till optimum level,AVC starts rising.It can be better understood with the help of a schedule and diagram given below.

AVERAGE TOTAL COST(ATC) or AVERAGE COST(AC)

Average cost refers to the per unit total cost of production.

AC = TC/Q (Q= Quantity of Output)

Average cost is also defined as the sum of AFC+ AVC

Like AVC, average cost also initially falls with increase in output. Once the output rises till optimum level, AC starts rising. It can be better understood with the help of a schedule and diagram.

MARGINAL COST (MC) : Marginal cost refers to addition to Total Cost when one more unit of output is produced.

MCn= TCn - TCn-1

OR

MC = Change in TC/ Change in units of output

MC IS NOT AFFECTED BY FIXED COST

The reason behind the 'U' shape of MC is the LAW OF VARIABLE PROPORTION.

Relation between AC and MC

- When MC is less than AC, AC fallswith increase in output

- When MC= AC, MC and AC intersecteach other.

- When MC is more than AC, AC rises with increase in output

AC depends on the nature of MC

- When MC curve lies below the AC curve, it pulls the latter downwards

- When MC lies above AC curve , it pulls the latter upwards

- Consequently, MC and AC are equal where MC intersect AC curve

Relationship between AVC and MC

- MC< AVC, AVC falls with increase in output

- MC = AVC , MC and AVC curves intersect each other

- MC> AVC, AVC rises with increase in output.

Relationship between AC and AVC

- AC is greater than AVC by the amount of AFC.

- The vertical distance between AC and AVC curves continues to fall with increase in output because the gap between them is AFC, which continues to decline with rise in output.

- AC and AVC curves never intersect each other as AFC can never be zero

- Both AC and AVC curves are 'U' shaped due to the law of variable proportion

- MC curve intersects AVC and AC curves at their minimum points

- The minimum point of AC curve lie always to the right of the minimum point of AVC curve.

Please go through the video links to understand the chapter better

https://www.youtube.com/watch?v=xZ6-h9Ib2LE

https://www.youtube.com/watch?v=Yr0eiVdK1RY

https://www.youtube.com/watch?v=uVFPB90gpWM&t=158s

good evening sir,KEVIN SUNIL PAPPAN 11B

ReplyDelete